Field Notes

The Biotechnology Renaissance Driven by AI

Quick summary

AI is starting to make biology look more engineerable, not because DNA is “just code,” but because biological sequences contain billions of years of statistical signal that transformers are unusually good at extracting. The near-term impact is probably fastest in discovery: target selection, protein design, molecule generation, safety simulation, and automated wet-lab iteration. Clinical trials remain the bottleneck, since biology and regulation still impose hard timelines, but the bigger opportunity is not merely making trials cheaper. It is sending better candidates into trials in the first place. If AI can even double clinical success rates from roughly 10% to 20%, the number of approved drugs per dollar of R&D could change dramatically. The current landscape splits into several buckets: Isomorphic/DeepMind as the flagship, AI protein and biologics design companies, end-to-end AI drug discovery platforms, pharma aggregators, autonomous labs, longevity companies, and custom designer therapies.

I’ve been focused lately on trying to understand what industries AI advances can easily diffuse into, and one of them worth exploring in depth is biotechnology.

DNA, RNA, and proteins form a literal symbolic chain, but the codon table was solved in the 1960s and needs no AI. What makes transformers work on biology isn’t that it’s “code”… it’s that evolution left billions of years of statistical signal in these sequences (conservation, co-variation), the shape of what survived, which is the kind of signal transformers are built to extract.

You may say yes, it’s a little bit more complicated than that because both RNA and proteins form three-dimensional structures and the DNA alone doesn’t tell you the biophysics of the interactions in vivo.

But without going into details (you can read the links below), it kind of looks like it’s going to work.

- evidence 1: DNABERT - reading regulatory signal from raw sequence

- evidence 2: Enformer - predicting gene expression from sequence

- evidence 3: Nucleotide transformer - genomic prediction at scale

- evidence 4: AlphaFold 3 - structure prediction, now with complexes

- evidence 5: RFdiffusion - generating novel proteins, not just reading them

Btw, Dario Amodei agrees with this.

How does drug discovery work today?

Let’s first review how drug discovery works today. As you probably know, it’s a long process with a lot of regulatory hurdles.

| Step | What happens | Typical timeline |

|---|---|---|

| 1. Target discovery | Find a disease mechanism/protein/pathway worth drugging | 6 months-3 years |

| 2. Hit discovery | Screen molecules/antibodies/etc. for anything that affects the target | 6 months-2 years |

| 3. Lead optimization | Improve potency, selectivity, solubility, toxicity, PK/PD | 1-3 years |

| 4. Preclinical | Cell/animal safety, toxicology, dosing, manufacturing prep | 1-2 years |

| 5. IND filing | Ask FDA for permission to test in humans | ~30 days FDA review |

| 6. Phase 1 | Small human safety/dosing study | months-1 year |

| 7. Phase 2 | Does it work in patients? More safety, dose finding | 1-3 years |

| 8. Phase 3 | Large pivotal trial vs placebo/standard care | 2-5 years |

| 9. NDA/BLA filing | Submit full evidence package for approval | 6-12 months review |

| 10. Launch + Phase 4 | Commercialization, long-term safety monitoring | ongoing |

So what is the longest part of this? Well, it’s clinical trials. It can take 5-9 years. Let’s make that even more clear in another table:

| Stage | What it means | Rough timeline |

|---|---|---|

| Discovery | Find target, hits, and optimize a lead drug candidate | ~2-6 years |

| Preclinical | Lab/animal safety, tox, dosing, manufacturing prep | ~1-2 years |

| IND | File to begin human testing | ~1 month FDA review |

| Clinical trials | Phase 1 safety, Phase 2 efficacy/dosing, Phase 3 large pivotal trials | ~5-9+ years |

| Approval | FDA review of NDA/BLA | ~6-12 months |

| Post-market | Monitor safety after launch | ongoing |

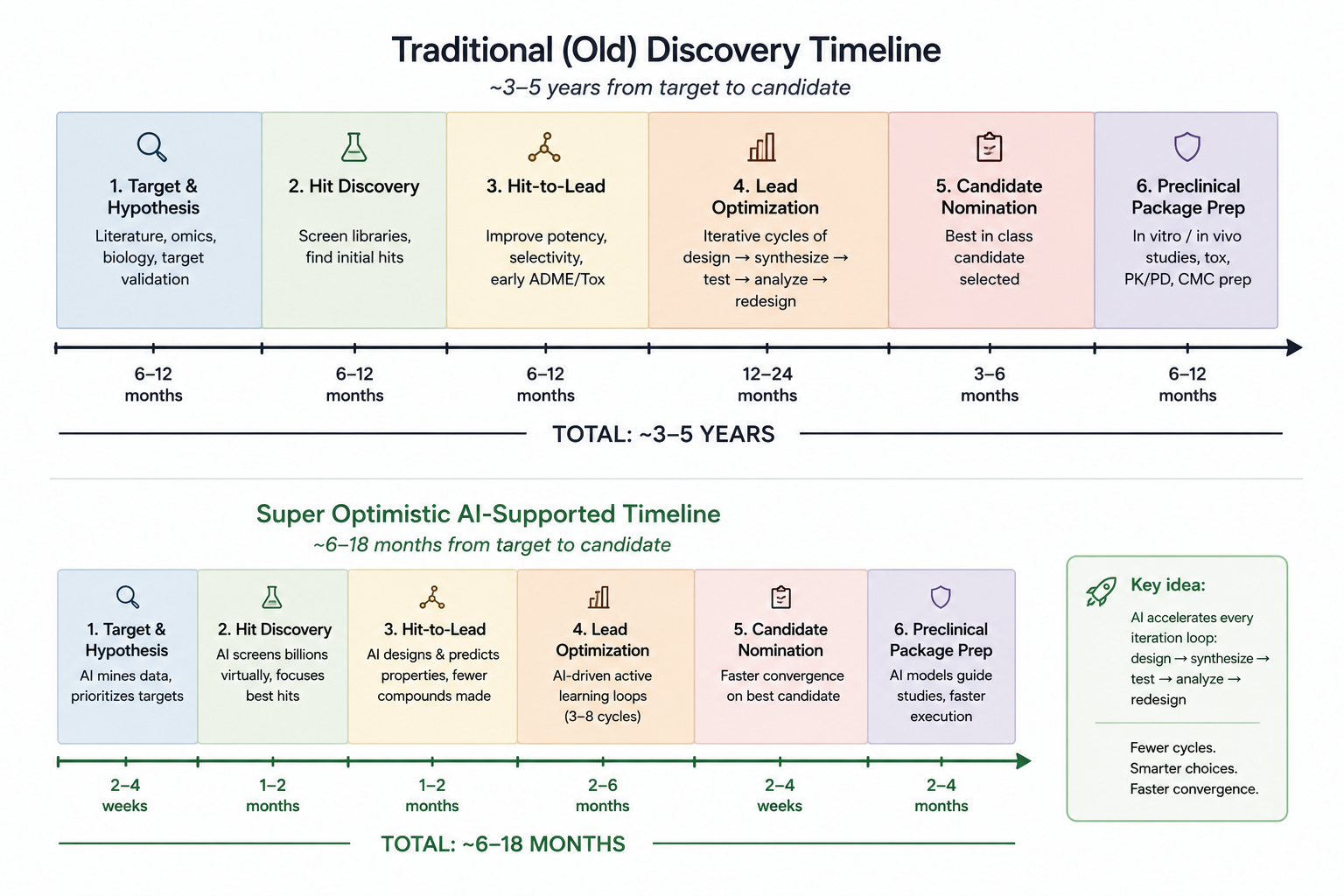

Discovery: How does AI change this?

The main thing to think about is this: how does AI speed up this timeline?

Well, ideally for everything before clinical trials, you might be able to iterate a lot faster. Maybe the conventional discovery and optimization phase (before trials) used to take 4.5 years on average. And if Insilico says they already got down to 30 months, it’s probably possible to compress this even further down to say 12 months or less. Really, a lot of the discovery and labwork should be able to be automated.

Trials: How does AI change this?

Discovery is the most obvious place AI will help produce drugs faster. When it comes to trials, it’s murkier.

But that’s not to say there are no benefits to be had here, although to be fair, it’s less dramatic. Let’s start with the components of a trial.

- Protocol design (how do you run the trial?)

- Site selection (which hospital, etc)

- Recruiting patients

- Treatment & monitoring

- Analyze

There are a lot more steps and components, but at a high level, those are the components. A lot of these can be optimized with straightforward SaaS application-style software and simple bits of data science.

I used GPT5.5 to help me build this table with some handwavy numbers and ideas around cost reduction and time speedup.

| Trial component | What happens | Typical time | Typical cost | AI time reduction | AI cost reduction | Why AI helps |

|---|---|---|---|---|---|---|

| Protocol design | Define endpoints, inclusion/exclusion, dose arms, visits, stats plan | 2-6 months | $0.5M-$3M | 20-40% | 10-25% | Simulate protocol feasibility, reduce dumb criteria, predict amendments |

| Site selection/startup | Pick hospitals/sites, contracts, IRB, training | 3-9 months | $20k-$100k+ per site | 15-35% | 5-20% | Pick sites with real eligible patients, avoid dead sites |

| Patient recruitment | Find, screen, consent eligible patients | 6-24+ months | Often 10-30% of trial cost | 20-50% | 10-30% | EHR mining, note parsing, biomarker matching, automated pre-screening |

| Enrollment/retention | Keep patients in the trial, reminders, visit completion | Runs through trial | High indirect cost | 10-25% | 5-20% | Predict dropout risk, automate reminders, reduce missed visits |

| Treatment/follow-up period | Dose patients and wait for safety/efficacy endpoints | Phase-dependent | Major cost driver | 0-25% | 0-15% | Hard to compress biology, but enrichment/digital endpoints can shorten some studies |

| Monitoring/site ops | Ensure protocol compliance, source data checks, site management | Runs through trial | ~10-15% of budget | 15-35% | 10-25% | Risk-based monitoring, anomaly detection, fewer manual visits |

| Data management | Clean data, reconcile queries, database lock | 3-9 months overlap/end | $0.5M-$5M+ | 25-50% | 15-35% | Real-time cleaning, automated query generation, EDC validation |

| Safety monitoring | Adverse event detection, narratives, medical review | Runs through trial | Meaningful ops cost | 10-30% | 10-25% | Faster AE triage, auto-drafted narratives, signal detection |

| Endpoint assessment | Imaging, pathology, biomarkers, clinical scoring | Runs through trial | Varies wildly | 10-40% | 5-25% | AI reads/scales imaging/pathology, reduces measurement noise |

| Statistical analysis | Interim/final analysis, subgroup analysis | 1-4 months | $0.2M-$2M+ | 20-50% | 10-30% | Faster TLFs, Bayesian/adaptive decision support |

| Regulatory package | CSR, NDA/BLA modules, FDA responses | 3-12 months | $1M-$10M+ | 25-60% | 15-40% | Drafting, consistency checks, automated tables, faster responses |

| Control arm | Placebo/standard-care comparator patients | Embedded in trial | Can be huge | 0-50% | 0-40% | Synthetic/external controls may reduce control enrollment in select cases |

Then, broken up into phases it helped me produce this table.

| Phase | Main purpose | Typical time | Typical cost | AI time reduction, optimistic | AI cost reduction, optimistic | Main AI lever |

|---|---|---|---|---|---|---|

| Phase 1 | Safety, dosing, PK/PD | 6-12 months | ~$1M-$7M | 10-30% | 5-20% | Better dose modeling, faster ops, safety monitoring |

| Phase 2 | Efficacy signal, dose finding | 1-3 years | ~$7M-$20M+ | 20-45% | 10-35% | Biomarker enrichment, adaptive design, faster recruitment |

| Phase 3 | Pivotal proof, larger safety database | 2-5 years | ~$20M-$100M+ | 15-35% | 10-30% | Site selection, recruitment, endpoint automation, fewer amendments |

| Submission/review prep | Assemble evidence package | 6-12 months | ~$1M-$10M+ | 25-60% | 15-40% | Automation of documentation, TLFs, QA, response drafting |

Most trials fail

AI can probably cut trial cost and time by 10-30% in ordinary cases, 20-40% in good cases, and maybe 50% in unusually AI-friendly cases.

But there is a bigger issue with trials:

Fewer than 10% of drugs that enter clinical development ever get approved, and the worst chokepoint is the Phase 2→3 transition — only ~30% of programs clear it.

On top of that, trials are the longest part of this process (remember: 5-9 years). There are simple fundamental physical & regulatory realities at play here that we can’t do much about - at least from line of sight with current technologies. Maybe you get down to 2.5 years, but probably not.

Improving failure rate: Ensuring efficacy & safety before trials

The big win is not shrinking trials; it’s selecting candidates that are more likely to pass the trial in the first place.

Trials fail due to safety or efficacy issues, and we should be able to use AI models and simulations during the discovery phase to better simulate both efficacy and safety.

Just to paint it clearly, if only 10% of drugs get through trials, if you were able to lift the likelihood of phase 2 trials and phase 3 trials passing by even double, to 20% (still a low pass rate), then overall you are going to have 2x the number of new drugs going out to the public every year for the same amount of capital invested.

But as we know, Jevons paradox means if you get more drugs overall, you probably get more capital in the hands of the drug makers, so it would accelerate this even further since they could invest the proceeds into even more drugs in the pipeline.

The current landscape.

1. Isomorphic / DeepMind / Google

This is the most interesting and promising place to pay attention. Unfortunately, Isomorphic is private, but they are backed by Google/DeepMind. By the way, DeepMind is the Google AI division behind AlphaFold, for which DeepMind researchers won the Nobel Prize in Chemistry in 2024.

Isomorphic just did a $2.1 billion Series B. No public results yet.

2. AI Protein / Biologics Design

| Company | Approx funding / size | One-line explanation |

|---|---|---|

| Xaira Therapeutics | $1B+ launch / Series A; some trackers show ~$1.3B raised | The mega-funded “build the Genentech of AI biology” company, combining ML, massive biological data generation, and drug development under Marc Tessier-Lavigne and a star-studded board. |

| Generate Biomedicines | Nearly $700M private equity raised pre-IPO; filed/planned ~$425M IPO, then reportedly raised ~$400M IPO in 2026 | Flagship’s protein-generation company, trying to program novel antibodies/proteins as therapeutics rather than merely discover them. |

| Chai Discovery | $70M Series A at ~$550M valuation; later $130M Series B, total ~$225M, reported ~$1.3B valuation | OpenAI-backed molecular design startup focused on predicting and reprogramming molecular interactions, with a strong antibody/protein-design angle via Chai-1/Chai-2. |

| EvolutionaryScale | $142M seed; acquired by Chan Zuckerberg/Biohub in 2025 per Reuters | Ex-Meta ESM team’s frontier protein language model company, best known for ESM3 and generative protein modeling, now folded into CZI/Biohub’s open protein-biology model push. |

| Profluent Bio | ~$150M total after $106M 2025 financing; valuation reportedly approaching $1B | AI-first protein design company using protein language models to design programmable biology, especially gene editors like generated Cas9-like systems. |

| Absci | Public, Nasdaq: ABSI; market cap recently around ~$1B; raised $50M public offering in 2025 and got $20M AMD PIPE in 2025 | Public generative-AI biologics company using wet-lab feedback loops to design antibodies and biologics, with clinical-stage programs but still very early revenue. |

| Cradle Bio | ~$100M+ raised, depending source | Protein engineering startup using ML to help design enzymes, antibodies, and other proteins with better stability, activity, and developability. |

| BigHat Biosciences | ~$100M+ raised | AI-guided antibody design company using active learning and wet-lab feedback to optimize therapeutic antibodies. |

| A-Alpha Bio | ~$80M+ raised | Uses massive experimental protein-protein interaction data to design and discover binders, especially for molecular glue / proximity biology style problems. |

| Tessera Therapeutics | $500M+ raised historically | Gene-writing company, more gene therapy than protein design, but adjacent because it depends on engineered biological machinery and delivery systems. |

| Nabla Bio | ~$25M-$50M range reported | Protein design company focused on de novo antibody-like binders against difficult targets, including GPCRs and transporters. |

| Adaptyv Bio | Smaller private, funding less transparent | Protein engineering automation company building foundry-like wet-lab infrastructure to test designed proteins faster. |

3. End-to-End AI Drug Discovery Platforms.

| Company | Approx funding / size | One-line explanation |

|---|---|---|

| Recursion Pharmaceuticals | Public, RXRX; cash ~$665M-$754M range recently; runway into early 2028 | The most “industrialized biology” public platform, using massive cellular imaging, automated wet labs, omics, and ML to map biology and generate drug programs. Recursion reported $753.9M cash/restricted cash at year-end 2025 and Q1 2026 commentary put cash around $665M, with runway into early 2028. |

| Insilico Medicine | Public, HKG:3696; recent market cap roughly HK$23.8B / ~$3B; IPO raised HK$2.277B / ~$293M | The AI-native target discovery + molecule design + clinical pipeline company, with Pharma.AI, PandaOmics, Chemistry42, a broad pipeline, and major Lilly validation. Its HK IPO raised HK$2.277B, and recent data showed market cap around HK$23.8B. |

| Schrödinger | Public, SDGR; 2025 revenue $255.9M; software revenue $199.5M; drug discovery revenue $56.4M | The physics-first computational chemistry platform, with real software revenue plus an internal/partnered drug-discovery portfolio. More “computational platform + pipeline” than full-stack AI biology, but very real. |

| Exscientia | Former public AI drug-discovery company; acquired by Recursion in all-stock deal, completed Nov. 2024 | One of the early AI-first small-molecule design companies, now folded into Recursion, bringing molecule design and precision oncology assets into Recursion’s wet-lab/phenomics machine. |

4. The big pharma companies

- Eli Lilly

- Novartis

- Johnson & Johnson

- Amgen

- AstraZeneca

- Roche / Genentech

- Sanofi

- Takeda

These companies buy / partner / license drugs from the smaller companies. They each have dozens of drugs in their pipelines and frequently capture most of the value in pharma. They have the distribution footprint and capital to get a drug over the finish line and out into the world.

These are all publicly tradable and pretty huge in terms of market cap.

5. Autonomous labs / science factories

Closed-loop experiment generation, robotic labs, cell therapy manufacturing, proprietary biological data. You need this layer to automate the discovery process end-to-end and tighten the feedback loop.

| Company | Public / private | Ticker / scale marker | One-line explanation |

|---|---|---|---|

| Lila Sciences | Private | ~$550M raised; >$1.3B valuation | Flagship-backed “AI Science Factory” company building AI-controlled robotic labs that generate proprietary experimental data across biology, chemistry, materials, energy, and semiconductors. Reuters reported a $115M extension in Oct. 2025, bringing total raised to $550M and valuation above $1.3B. |

| Cellares | Private | ~$612M total funding; reported ~$1.4B valuation | Automated cell-therapy manufacturing company building Cell Shuttle factory systems to industrialize CAR-T/cell therapy production. Its Jan. 2026 $257M Series D brought total capital funding to about $612M; Forge reports a May 2026 Series D-1 valuation around $1.4B. |

| Ginkgo Bioworks | Public | NYSE: DNA; market cap ~$600M | Public synthetic-biology foundry pivoting hard toward autonomous labs; important as both a real infrastructure player and a cautionary tale after the SPAC-era valuation collapse. Yahoo Finance showed market cap around $597M, and Ginkgo’s Q1 2026 release says its Nebula autonomous lab is the world’s largest and that it aims to double its size in 2026. |

| Emerald Cloud Lab | Private | ~$151M-$152M raised; Forge shows ~$336M post-money in 2025 round | Remote robotic cloud lab that lets scientists run chemistry/biology experiments through software. Funding sources put total raised around $151M-$152M, with Forge showing a July 2025 Series C-1 post-money valuation of about $336M. |

| Automata | Private | ~$145M-$177M raised; $45M Series C in 2026 | Lab automation hardware/software company building modular, AI-ready robotic lab infrastructure for pharma and biotech. Automata announced a $45M Series C in Jan. 2026, while funding trackers put total raised roughly in the $145M-$177M range. |

| Culture Biosciences | Private | ~$100M-$107M+ raised; Series C in 2025 undisclosed | Cloud-connected bioreactor / bioprocess development company, making fermentation and biologics process development more programmable and data-rich. The company said it had raised over $100M after its 2021 Series B, and trackers put total funding around $107M after its 2025 Series C. |

| Synthace | Private | ~$77M-$95M raised depending source; $35M Series C in 2021 | Life-sciences R&D automation software company that helps scientists design, automate, and analyze biological experiments across lab instruments. Synthace announced a $35M Series C in 2021; trackers put total funding roughly $77M-$95M. |

| Strateos | Private | ~$73M-$108M raised depending source; $56.1M Series B in 2021 | Earlier robotic cloud-lab / SmartLab platform for remote automated R&D experimentation. Its 2021 Series B was $56.1M, and funding trackers put total raised in the ~$73M-$108M range. |

6. Longevity / adjacent biology

Adding this because it’s one of the aspects of AI that is frequently mentioned by futurists: AI might help us solve aging, which is complex and multivariate.

| Company | Approx funding / size | One-line explanation |

|---|---|---|

| Altos Labs | ~$3B raised | The giant cellular rejuvenation / partial reprogramming moonshot, trying to restore cell health and resilience rather than treat one disease at a time. |

| Calico | ~$2.5B committed historically | Alphabet’s aging-biology lab, secretive and basic-science-heavy, trying to understand aging mechanisms and translate them into therapeutics. |

| Retro Biosciences | $180M initial Altman backing; raising/raised much more, valuation reported ~$1.8B to potentially $5B chatter | Sam Altman-backed longevity company aiming to add ~10 healthy years via autophagy, stem-cell, plasma, and reprogramming approaches. |

| NewLimit | $435M Series C led by Founders Fund; reported valuation around $3.1B | Brian Armstrong / Blake Byers company using AI-guided epigenetic reprogramming to make old cells behave younger. |

| BioAge Labs | Public, BIOA; raised $198M IPO, then ~$132M follow-on in 2026 | Human-aging-data company now mostly a public metabolic/inflammatory disease biotech, with less pure “longevity moonshot” exposure than the branding implies. |

| Life Biosciences | ~$230M-$260M total reported; $80M Series D in 2026 | Partial epigenetic reprogramming company whose ER-100 became an FDA-cleared cellular rejuvenation therapy candidate for human optic-neuropathy trials. |

| Cambrian BioPharma | ~$160M disclosed by company in 2022; some trackers estimate higher later | Longevity holding-company / pipeline-builder model, backing therapeutics against specific biological drivers of aging rather than one platform. |

| Loyal | Over $250M total after $100M Series C | Dog longevity company, probably the cleverest regulatory wedge because companion animals offer shorter trials and a real “lifespan extension” endpoint. |

| Rubedo Life Sciences | ~$52M-$54M raised; $40M Series A | Senescence / pathological aged-cell targeting company, more grounded in age-related disease than “live forever” rhetoric. |

| Turn Biotechnologies | ~$29M-$30M raised | mRNA-based partial reprogramming company trying to rejuvenate specific tissues without full dedifferentiation. |

| Gero | ~$13.5M-$20M reported, depending source | Physics/AI-flavored aging company modeling human aging dynamics from large-scale data to find intervention points. |

7. Custom Designer Therapies

Can you get a drug treatment that specifically solves, e.g., your specific cancer?

| Company / program | Public / private | Ticker / scale marker | One-line explanation |

|---|---|---|---|

| Moderna + Merck, V940 / mRNA-4157 / intismeran autogene | Public pharma partnership | MRNA ~$20B+ mkt cap; MRK ~$200B+ mkt cap | The flagship individualized cancer-vaccine program: sequence the patient’s tumor, algorithmically select neoantigens, manufacture a custom mRNA vaccine, and combine with Keytruda. Now in Phase 3 melanoma and NSCLC trials. Merck describes V940 as encoding up to 34 neoantigens selected from the patient’s tumor mutational signature. |

| BioNTech + Genentech/Roche, autogene cevumeran | Public pharma partnership | BNTX public; Roche/Genentech public via ROG.S / RHHBY | Personalized mRNA neoantigen vaccine most famous for pancreatic cancer data from MSK, where a small early trial showed immune responses and delayed recurrence signals; now being tested in randomized Phase 2 |

| n-Lorem Foundation | Nonprofit | Not investable; scale marker: 50th personalized ASO patient treated by Apr. 2026 | The purest N-of-1 model: custom antisense oligonucleotide medicines for nano-rare patients, provided free for life, built around the “milasen” lineage of individualized ASOs. n-Lorem says the 50th nano-rare patient had received a personalized ASO by April 2026. |

| Creyon Bio | Private | ~$40M raised; Lilly deal $13M upfront + up to ~$1B milestones | AI-designed oligonucleotide company trying to industrialize custom or semi-custom RNA-targeted medicines, with Lilly validating the platform through a multi-target collaboration. |

| Ionis Pharmaceuticals | Public | IONS, ~$5B-$7B-ish mkt cap recently | Not usually framed as “AI custom therapy,” but Ionis is the foundational ASO platform company behind the technical lineage that makes individualized antisense plausible. |

| Sarepta Therapeutics | Public | SRPT, market cap highly volatile | Not N-of-1 exactly, but exon-skipping / genetic-medicine logic points toward increasingly mutation-specific therapies for muscular dystrophy and rare disease. |

| CRISPR Therapeutics / Vertex, Casgevy | Public/public | CRSP public; VRTX mega-cap | Not individualized design per patient, but clinically important “edit the patient’s own cells” therapy, a stepping stone toward bespoke genetic interventions. |

| Caribou / Beam / Prime Medicine | Public gene-editing companies | CRBU / BEAM / PRME | Not custom therapies yet in the strict sense, but their editing platforms could become part of the designer-therapy stack if variant-specific editing becomes practical. |

Conclusions

The clearest near-term win from AI is discovery: faster targets, molecules, and design loops. Speed to trial, basically.

But the deeper point is about trials. They’re usually framed as an immovable wall, and AI does little to shorten them.

That framing misses the real lever: most drugs fail in trials not on speed but on efficacy: the biology was wrong going in. So trials are a filter: now imagine if 90% of the drugs going into trials passed instead of 10%?

I’m not saying we can get there quickly, but what if we can just double the pass rate to 20%?

You would double the number of drugs coming to market and further accelerate the industry.

Investment implications

My uncomfortable conclusion is that the science thesis is clearer than the investment thesis.

- The highest-purity companies are mostly private.

- The public pure plays are risky clinical-stage biotechs.

- The safest public companies are big pharma and Alphabet, but their AI-biology exposure is diluted.

| Investment bucket | Public names you can actually buy | Private names that would be amazing to own if accessible | Exposure purity | Investment clarity | My read |

|---|---|---|---|---|---|

| Frontier AI biology / drug design | GOOGL via DeepMind/Isomorphic, GENB Generate Biomedicines | Isomorphic Labs, Xaira, Chai Discovery | Medium-high scientifically, low-medium as public exposure | Medium | This is probably the most important part of the stack, but the best assets are private or buried inside Alphabet. Generate is newly public and much purer, but still clinical biotech risk. |

| End-to-end AI drug discovery platforms | RXRX, SDGR, ABSI, 3696.HK Insilico | Genesis, Iambic, other AI-native drug discovery platforms | High | Medium | This is the cleanest public AI-biotech basket. Schrödinger is the most grounded software/business model; Recursion and Insilico are higher-purity but need clinical proof. |

| Big pharma value capture | LLY, MRK, NVS, RHHBY/Roche, AZN, JNJ, AMGN, SNY | N/A | Low-medium | High | If AI improves discovery productivity, big pharma may capture a lot of the value through licensing, acquisitions, trials, manufacturing, and commercialization. Less pure, but probably the safest way value shows up. |

| Custom designer therapies | MRNA, BNTX, IONS, CRSP, BEAM, PRME, VRTX, MRK | Creyon Bio; n-Lorem is important but nonprofit | Medium | Medium | Personalized cancer vaccines and oligo/gene therapies are one of the most tangible “custom medicine” paths. V940 is the flagship, but public exposure is diluted inside Moderna/Merck and BioNTech/Roche-style platforms. |

| Autonomous labs / science factories | DNA Ginkgo, with caveats | Lila Sciences, Cellares, Emerald Cloud Lab, Automata | High conceptually, low publicly | Low-medium | This layer should matter because AI needs automated wet-lab feedback. But Ginkgo is the cautionary public comp, and the best-looking new companies are private. |

| Longevity / aging biology | BIOA, plus indirect GOOGL via Calico | Altos, Retro, NewLimit, Life Biosciences, Loyal | High conceptually, low publicly | Low | This is the most exciting narrative bucket and the least cleanly investable. Most of the best assets are private, while the public names are narrow or speculative. Treat mostly as a watchlist. |

| AI-biotech picks and shovels | TMO, DHR, A, ILMN, WAT, TECH, plus cloud/GPU names indirectly | Private lab automation and data-infrastructure vendors | Medium | Medium-high | The less glamorous angle: if AI biology accelerates experimentation, demand rises for sequencing, lab automation, assays, instruments, data infrastructure, and compute. This may be less pure but more durable. |

| Private-market moonshots | Not directly public | Isomorphic, Xaira, Lila, Cellares, NewLimit, Chai, Creyon | Very high | Low unless you get access | The best pure plays are mostly private. If they IPO at sane valuations after real clinical or commercial proof, they may become the most interesting opportunities. Until then, they are more watchlist than portfolio. |